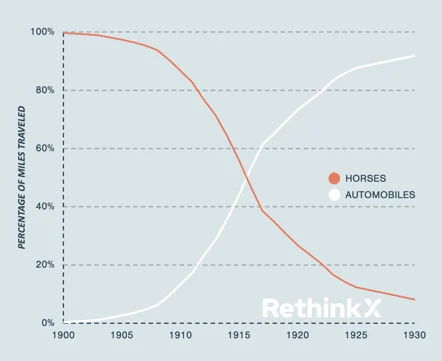

I want to share a chart. It shows the horse-to-automobile transition in the United States between 1900 and 1930. In 1910, horses still accounted for roughly 85% of miles traveled. The automobile was real, but marginal.

Now imagine there’s a hay crisis in 1910. Prices spike. Supply is disrupted. A journalist writes: “What automotive transition? The world still runs on horses.”

Technically accurate. Completely wrong about what was already underway.

That’s basically the argument an article in The Globe and Mail made today, using a Middle East oil shock as evidence that the energy transition is a myth. Fossil fuels are still 81% of primary energy supply, they note. Only six percentage points down from 1973. Transition debunked.

That 81% figure isn’t even the right number—once you account for how inefficient fossil fuels are compared to clean energy, the real figure is closer to 68%, meaning zero-carbon sources already meet roughly one third of global energy demand, not one fifth. (Michael Liebreich unpacks this thoroughly.)

The deeper problem, though, is that this is exactly what transitions look like from the inside. They’re slow, then they’re sudden. The S-curve doesn’t announce itself—until it does.

And yet this same chart gets misread from both ends. On one side, an oil shock becomes proof the transition is a myth. On the other, the existence of the S-curve becomes justification for demanding we shut down all fossil fuel infrastructure tomorrow. Both are wrong. In the United States, the horse-to-car transition took more than thirty years of messy, uneven, disruptive change—and the people who thought it would happen overnight were just as mistaken as the ones who insisted it was not really happening.

Here is what the Globe and Mail piece misses entirely: this crisis is not just evidence of our current dependence on oil. It could potentially accelerate the very transition it claims isn’t happening.

Every country watching oil prices spike 25% in a week is asking the same question: how do we reduce this exposure? In the past, there was no real answer. You were dependent on fossil fuels because there was no credible alternative at scale. That is no longer true. Solar, wind, and electrification have crossed cost thresholds to open possibilities that simply did not exist a decade ago. For the first time in history, countries have a genuine choice — and a geopolitical crisis of this kind is precisely the moment they start making it.

We have seen this before. The oil shocks of the 1970s accelerated nuclear buildout in France and efficiency standards across Europe. This crisis will do the same—potentially faster, because the alternatives are cheaper, more mature, and more widely available than they have ever been. The countries that move decisively will reduce their exposure to the next shock. The countries that don’t will have this conversation again.

Canada deserves a more serious conversation than either of these positions.

We are in the middle of a multi-decade transition. The direction is not seriously in question. The pace, the scale of disruptions, and how costs and benefits are distributed as the transition proceeds absolutely are.

For Canada, that means extracting value from our resource endowment right now and not apologizing for it. But it also means investing in the new energy economy that is emerging as a foundation for prosperity as this century advances. We can think of that as a serious risk mitigation strategy for a world where today’s assets may face structural headwinds within their own investment horizon. That’s not environmentalism. That’s fiduciary responsibility.

We need industrial policy built on how transitions actually work—not ideology dressed up as pragmatism, and not denial dressed up as realism.

Moe Kabbara, CEO